AFP PHOTO / DANIEL MIHAILESCU

This article has been published in collaboration with the Bilten regional platform.

The illusion of the “private vs. public” opposition

A flurry of irate opinions, fuming comments, and angry analyses have emerged in Romania’s liberal press once the Social-Democratic Prime-Minister, Mihai Tudose, announced in late August, under rather vague terms, his Cabinet’s intentions to reform the pension system. The debate developed into a strange public fray, mixing economic fears, fiscal fatalism, and demographic concerns; a discursive potion which is unfortunately representative of the manner in which the pension system has been discussed in recent years, both in Romania and outside of it.

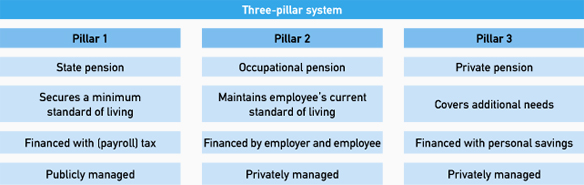

Like most Eastern European countries, since 2008 Romania has instituted a three-pillar pension system: the bulk of social security contributions going into the public system (the first pillar), with the mandatory private funds gathering 5.1 % of contributions, and a third voluntary private pillar emerging as well. The Prime-Minister’s vague statements seemed to imply a sizeable reduction in the role played by mandatory private pension funds, the so-called second-pillar, despite the fact that up until now most governments have promised to increase its size rather than reduce it. The plans were received by the press as another catastrophic intervention by the state into the private realm, a mortifying return to a state-dominated social security system, which would threaten the gains made so far in liberalizing the economy. Discussions about the “nationalization” of pension funds thrived, even though there was hardly any mention of such a move by the government: the boldest proposals simply wanted to reduce its size from 5.1% to 2.5%, or simply to make the mandatory private system voluntary. Various organizations, representing Romanian investors and entrepreneurs, expressed their dismay, accusing the government of playing with “our future” in order to solve passing budgetary problems. In an outburst of lyrical Hayekian prose, a Central Bank economist could not help in seeing the reforms as an expression of an age-old desire by Romanian politicians to increase the sway of the state over the lives of citizens, controlling every course of their lives. Such tacky, gauche ideologizations of the matter, along with the general brouhaha created by the Prime-Minister’s statements are somehow symptomatic of the way that the Social-Democratic coalition in power has managed to communicate its program. It’s also representative of the way in which it has been received by the opposition and in the public sphere.

On the one hand, the Prime-Minister’s statements were a perfect exercise in disastrous PR strategies: they came totally out of the blue, without being backed by any policy report or concrete analyses, let alone any feasible solutions to problems nobody knew they were having. For better or for worse, the Romanian private pension funds have not elicited any problems similar to the ones faced by Slovakia in 1998 or other failed attempts to introduce mandatory private retirement plans. Prior to the recent debate, there was hardly any mention of the need to give the three-pillar pension system a face-lift. And even now, the only justification for the government’s proposals is the vague accusation that private fund managers are profiteering from their position

More importantly, however, the government critics managed to frame the issue as the difference between private and public management, between state and market: a simplistic but efficient way to win any economic debate, even now, so many years after the Great Recession. The question became which one of the two systems is the most effective: the old “pay-as-you-go” (PAYGO) social security system where pension funding depends on inter-generational solidarity, demographic changes, and fiscal policies or the private system, where the risks are more individualized and there is no inter-generational dependence: the pension depends solely on one’s contributions to one’s personal retirement fund. From this abstract perspective, the answer seems pretty simple, especially as the public pillar faces a real and pressing deficit, exacerbated by the reduced number of employees and the increasing number of pensioners depending on it. For every ten employees contributing to the system there are nine pensioners. The number of contributing wage-earners has shrunk from 8.5-million in 1990 to 4.8-million today. It’s hard, from this abstract vantage point, to avoid the feeling of a fatalistic demographic conundrum affecting the central piece of post-war welfare, the PAYGO pension system. This worrisome rationale has managed to mix fiscal concerns with demographic fears about an aging population, which allegedly would make the system untenable in the long run. From this vantage point Romania is just another example of the insurmountable hurdles facing the post-war consensus built upon the PAYGO system, while private pension funds are the unavoidable solution for future generations of workers. Out of this comparison between the two pillars, the public and the private, the PAYGO system appears as the poorer cousin, with a permanent deficit, bound to rise because of demographic reasons and solved solely through cheap budgetary tricks.

The recent history of the pension system: demographic fatalism or low wages?

What this abstract comparison, always brought up by the press, fails to mention however, is the historical circumstances that made the private pillar relatively stable, while the public one is still dealing with a financing crisis. First and foremost, it is hard to see the shrinkage of employed contributors as simply the result of aging, an iron demographic law: gigantic waves of labour migration have played a significant role in this reduction, and these were the result of low income levels rather than a natural process. More than two million Romanians are working abroad legally, almost half of the current number of social security contributors. Similarly, as it has been noted, an economy strongly depended upon the allure of low wages for foreign investors (FDI), can hardly deal with the funding costs of an efficient pension system. The share of wages as part of the overall aggregate product is one of the lowest in Europe and this has a gigantic impact upon the social security system. Depressed wages trigger new waves of economic migrants and, consequently, the loss of significant number of contributors. It pushes old workers out of the labour market, forcing the pension system to take over the burden. In the same vein, it leads to meagre social security contributions while down-sizing the fiscal revenues which might come from internal consumption. It is difficult to manage an efficient welfare system without acceptable wage levels. Rather than simply the result of demographic changes, the current problems of the PAYGO system are a direct result of economic strategies based much too often on the appeal of low wages for capital owners.

What this abstract comparison, always brought up by the press, fails to mention however, is the historical circumstances that made the private pillar relatively stable, while the public one is still dealing with a financing crisis. First and foremost, it is hard to see the shrinkage of employed contributors as simply the result of aging, an iron demographic law: gigantic waves of labour migration have played a significant role in this reduction, and these were the result of low income levels rather than a natural process. More than two million Romanians are working abroad legally, almost half of the current number of social security contributors. Similarly, as it has been noted, an economy strongly depended upon the allure of low wages for foreign investors (FDI), can hardly deal with the funding costs of an efficient pension system. The share of wages as part of the overall aggregate product is one of the lowest in Europe and this has a gigantic impact upon the social security system. Depressed wages trigger new waves of economic migrants and, consequently, the loss of significant number of contributors. It pushes old workers out of the labour market, forcing the pension system to take over the burden. In the same vein, it leads to meagre social security contributions while down-sizing the fiscal revenues which might come from internal consumption. It is difficult to manage an efficient welfare system without acceptable wage levels. Rather than simply the result of demographic changes, the current problems of the PAYGO system are a direct result of economic strategies based much too often on the appeal of low wages for capital owners.

On the other hand, Romania, along with the Czech Republic, is part of a second generation of pension privatizers and this left a giant mark upon its social security system, increasing the stability of the private pillar. Responding to the pressure of the World Bank and its expert teams, Romania has shown interest in creating a private pension sector since the 1990s. Nevertheless, the Social-Democratic forces dominating the transition have constantly postponed any concrete measures. Theirs was a rather bold move of policy restraint in a period of excessive enthusiasm for private pension funds. Centred around the World Bank and building upon the Chilean example of the 1980s, private pension funds had become by the 1990s a global policy tool, backed by powerful international actors and pressure groups. From 1981 until 2005 the introduction of private retirement funds underwent impressive growth, with Latin America leading the pack, followed by Central and Eastern Europe, but also countries in Sub-Saharan Africa and Western Europe (England, Germany, the Netherlands, etc). Within this context of neoliberal enthusiasm, most Central and Eastern European countries tried, in Mitchell Orenstein’s words, to out-liberalize the EU, featuring even more radical privatization reforms of their pension systems. The Romanian Social-Democrats showed a great deal of circumspection regarding these innovations in spite of paying lip-service to the general rhetoric favouring private retirement funds. Ironically, the first concrete steps in such a direction came only in 2008, when the global enthusiasm about private funds was already on the wane. After 2005 even the World Bank tried to tone down its recommendations, as the early reforms in Central and Eastern Europe were beginning to bear their sour fruits. For these reasons, when in 2008, right before the crisis, the Romanian authorities finally established a second private pillar, they could actually learn from and at least partly avoid the mistakes that had marred such initiatives in other regional countries: Slovakia, Hungary, etc. It was this belatedness, in a way, that ensured the relative success of the private pension funds. Thus, they could organize a more efficient monitoring system for private pension funds, while also adopting a strategy that would not dramatically affect the public system. It was this later aspect, however, which still remains the most problematic.

Transition costs: the public burden of private pension funds

Contrary to the opinions aired in the Romanian public sphere, the relationship between the public and the private pillar is not just one of abstract comparison, of autonomous funding systems which hardly influence each other and where the question is simply which one benefits the contributor more, ensuring a happy retirement: the PAYGO system of inter-generational dependence, or the individualistic private one. The introduction of private retirement funds already impacts dramatically the public system, leading to gigantic financial losses. Thus, it diverts a significant amount of money out of the public pension system into private hands; money which can only be recovered in the long run, in decades rather than years. Dealing with these transition costs, as they have been called, has been one of the main concerns of public authorities since the 1990s. The solutions have varied: increasing fiscal revenues, cutting down on pensions (austerity measures) or simply through the downright privatization of public assets (as was the case with Poland). The budgetary problems that came with the 2008 crisis made the financing issues even starker, especially as regional countries now had to play by the rules of the Maastricht criteria: a budget deficit which could not exceed 3% of the GDP.

Contrary to the opinions aired in the Romanian public sphere, the relationship between the public and the private pillar is not just one of abstract comparison, of autonomous funding systems which hardly influence each other and where the question is simply which one benefits the contributor more, ensuring a happy retirement: the PAYGO system of inter-generational dependence, or the individualistic private one. The introduction of private retirement funds already impacts dramatically the public system, leading to gigantic financial losses. Thus, it diverts a significant amount of money out of the public pension system into private hands; money which can only be recovered in the long run, in decades rather than years. Dealing with these transition costs, as they have been called, has been one of the main concerns of public authorities since the 1990s. The solutions have varied: increasing fiscal revenues, cutting down on pensions (austerity measures) or simply through the downright privatization of public assets (as was the case with Poland). The budgetary problems that came with the 2008 crisis made the financing issues even starker, especially as regional countries now had to play by the rules of the Maastricht criteria: a budget deficit which could not exceed 3% of the GDP.

For these reasons, following the crisis, almost every country in Eastern Europe tried to reduce the size of its second pillar, bringing the money back into the public system. The most extreme measures were taken by Hungary, which simply decided to nationalize the private pension funds, partly to service its outstanding debt. For the Romanian right-wing authorities running the show during the crisis, the most appropriate response was austerity, while the second pillar increased in size from 2.5% to the current 5.1%. These transition costs, however, remain a hidden topic for pundits and commentators, whose analytical imagination has been confined to the idea of perfect competition between two autonomous systems, the private and the public one, which never communicate with one another, and hardly influence each other.

And yet the magnitude of these budgetary problems will probably increase very soon, making these transition costs more salient than ever. Despite their rather confused economic program, the Romanian Social-Democrats, who are now in power now, are following a Neo-Keynesian policy which, through tax reduction and increased wages, can easily lead to larger budget deficits, untenable under the Maastricht criteria. If the social security contributions that are now being channelled into private pension funds are not reduced, the public pillar will face real financing problems. Beyond demographic fears and fantasies, there are real economic decisions that have to be made.

Dan Cîrjan is a PhD candidate in the Department of History of the Central European University in Budapest. His research interests include economic sociology, labour studies and the political economy of Eastern Europe, with a focus on the first decades following the Great Depression. He is currently working on his doctoral dissertation on the restructuring of the Romanian financial system after 1929, with an emphasis on the state’s public debt and the private debt of the Romanian rural communities.

Dan Cîrjan is a PhD candidate in the Department of History of the Central European University in Budapest. His research interests include economic sociology, labour studies and the political economy of Eastern Europe, with a focus on the first decades following the Great Depression. He is currently working on his doctoral dissertation on the restructuring of the Romanian financial system after 1929, with an emphasis on the state’s public debt and the private debt of the Romanian rural communities.